I want to review my long-term investment strategy and educate others on basic investing techniques. The goal of this post is to introduce a passive investment strategy.

Most people don’t have the time nor the inclination to review their investments frequently. Passive investment strategy allows the flexibility of a little work in the beginning and smooth sailing in the long run.

What I’ll Cover

- Why should you invest instead of putting your cash in a savings account?

- What type of investments should you make?

- How should you go about passive investing?

- When is the right time to start investing?

Why?

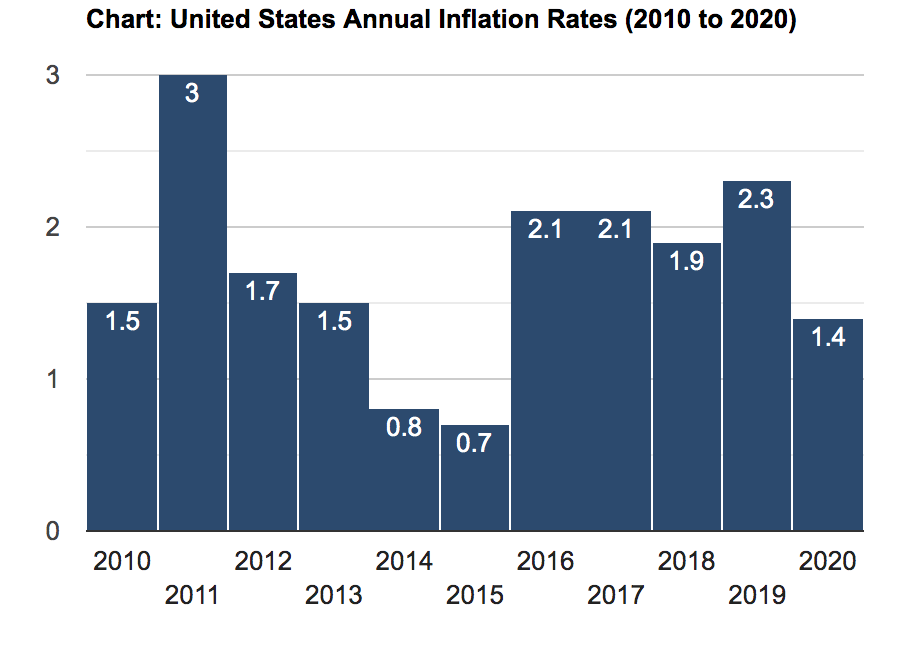

Inflation is killing your gains.

The U.S government is printing money every year.

The interest you earn in your savings account doesn’t eclipse the inflation rate, so you end up having less purchasing power in the long term. COVID-19 has accelerated inflation, so all things considered, holding the money in your bank account is not advised.

Where else can you allocate your money? Let’s go through a few investment options.

What?

Real Estate can be lucrative long term, but you need a large amount of capital to start. Real Estate is also not as passive as you’d think. You’re tied to a costly asset and regularly need to allocate funds into maintenance.

Government Bonds and Treasury Bonds are extremely low-risk investments that don’t give you a great return rate. Once you accrue more income and get older, it makes sense to diversify your assets with government bonds but hold off for now.

The Stock Market lets you invest in individual companies with the hope that the company rises in value. No one can predict how the stock market moves! Even pros who do this for a living get it wrong—a lot.

Warren Buffet won a 10-year bet bet where he proved that the S&P1 had better returns than any Hedge Funds2 who meticulously pick the best stocks (and charge you expensive fees to boot).

So how do you ‘beat’ the stock market? No one can predict if stock A or B will go up or down, but if you follow the stock market’s history, you’ll notice two trends.

First, the stock market has cycles where it goes up and down. Second, over the long run, the trend is for the market to go up! The market goes up over long periods due to human productivity. If you want to understand how the economy and economic cycle works, Ray Dalio’s explanation is terrific. I’ll touch more on the first trend later when I talk about when to buy but now let’s focus on the second trend. If you know the general stock market will go up over the long term, how can you benefit? Invest in index funds, which are a pool of stocks. You can balance out your risk and not put all your eggs in one basket. If one company fails, you don’t lose all your money because it’s a small portion of the fund. On the flip side, if one of the portfolio companies booms, you won’t get a huge upside. The goal here is to balance risk and reward. Over the long run, there’s virtually no risk and quite a good reward. Here are a list of common index fund and their yearly returns3

| Fund Names | 1-yr | 3-yr | 5-yr | 10-yr |

| VFIAX | 18.37% | 14.14% | 15.18% | 13.85% |

| VTSAX | 20.99% | 14.49% | 15.42% | 13.78% |

| SWPPX | 18.39% | 14.15% | 15.16% | 13.81% |

| SWTSX | 20.71% | 14.37% | 15.32% | 13.72% |

How?

Now that you’ve warmed up to the idea of investing in mutual funds, where should you go to invest? These days you can go to several online brokerages that make investing easy. A few of these are:

Every broker listed offers index funds, so don’t worry too hard about which you pick. They each have minute differences that you can read up on with a quick google search.

When?

You don’t want to buy at the market’s peak and should look to buy when the market swings downward and stocks are “cheap.” Of course, you have no idea when that is, and most people don’t either. Instead of timing the market, dollar cost average instead. Dollar-cost averaging (DCA) is an investment strategy in which an investor divides up the total amount to be invested across periodic purchases to reduce the impact of volatility on the overall purchase. I put in a % of my income every week into my index funds, no matter the price. In the long run, prices average out, and I’ll be taking advantage of the trend I mentioned earlier (Markets, in the long run, go up). The best part about dollar-cost averaging is that most brokerages allow you to set this up to run automatically. You don’t even need to check your stocks! Set the amount and frequency and leave it alone. Maybe after getting a raise, adjust the amount/frequency to be a % of your income (Strive to allocate 30%+ of your income to passive investing).

Don’t take out the money for at least 3-5 years. Allow compound interest to work its magic and exponentially increase your net worth.

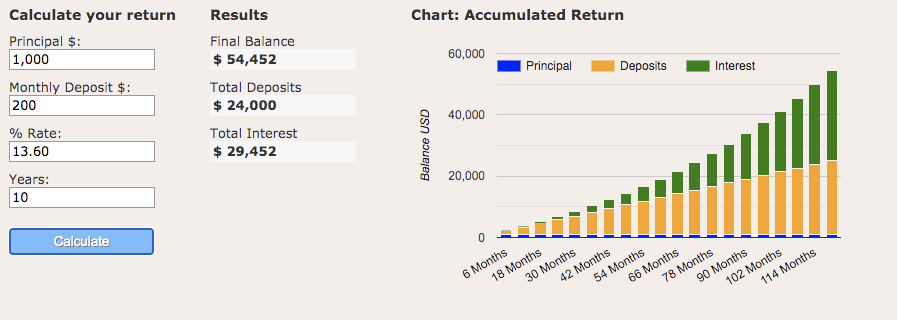

In the example below, If I started with 1K and gradually placed $200 of my income a month in an index fund with YoY gains of 13.6% (S&P 500 average over the last ten years). My final balance is $54K with $30K of compounding interest in addition to my $24K of deposits.

Conclusion

Dollar-Cost Averaging in index funds is the most practical way to invest your income passively. You can be a bit more proactive if you’re interested. Read up on how to evaluate companies. Many financial books, videos & articles are out there for free! Make your own decision but understand that you’re essentially gambling if you are looking for short-term profit. It’s worth waiting long term, playing it safe, and reaping huge gains with compound interest.

Footnotes

- S&P 500: The S&P 500, or simply the S&P, is a stock market index that measures the stock performance of 500 large companies listed on stock exchanges in the United States. It is one of the most commonly followed equity indices

- Hedge Fund: Hedge funds are alternative investments using pooled funds that employ different strategies to earn active returns, or alpha, for their investors

- Common index funds Yearly Returns: Avg year returns. SWTSX Example